UK-EU Trade: Links to Key Data

John Sydenham

A Free Trade Agreement was signed between the EU and UK in 2021. It had been applied provisionally since January 2021 and became law in May 2021. This ensures that there are no tariffs and quotas between the UK and the EU. The UK public is largely unaware of its existence. It has ensured that UK trade with the EU has continued along the same trend as before Brexit and COVID.

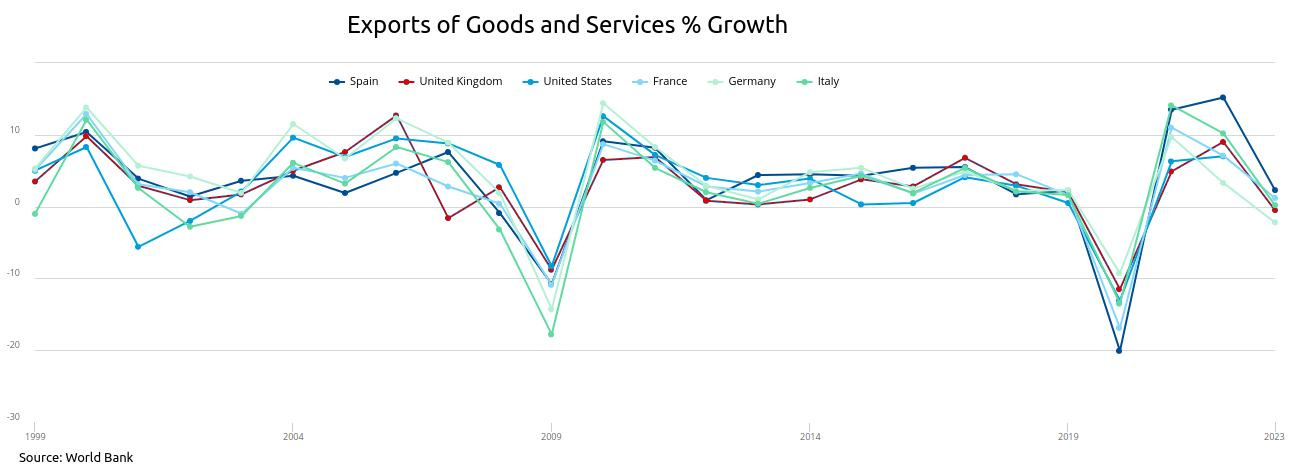

How well has the UK done relative to other large economies in the EU? Was there any change in 2016 or 2021 in the rate of growth of imports and exports compared with other countries?

The two major events in the global economy over the past 25 years were the Banking Crisis and COVID. Notice how Brexit does not register. Neither the EU Referendum nor the final agreements on 1 January 2021 had any effect. The UK is within the trends of other major EU economies, neither outperforming nor underperforming the norm.

Brexit was invisible at the level of UK global trade. The EU is responsible for 42% of UK exports and 52% of UK imports (UK Government: Statistics on UK trade with the EU) so it is possible that improved global trade is hiding worsening EU trade.

What happened to UK-EU trade?

Here are links to the UK Office of National Statistics figures for UK-EU Trade plus graphs of what happened. If you click on the headings (such as Balance of Trade in Goods and Services with EU, Exports of Goods to EU etc) you will be able to see the original source data. The source data appears as quarterly figures but has options above each graph to see the annual figures. This allows you to check the original data for yourself.

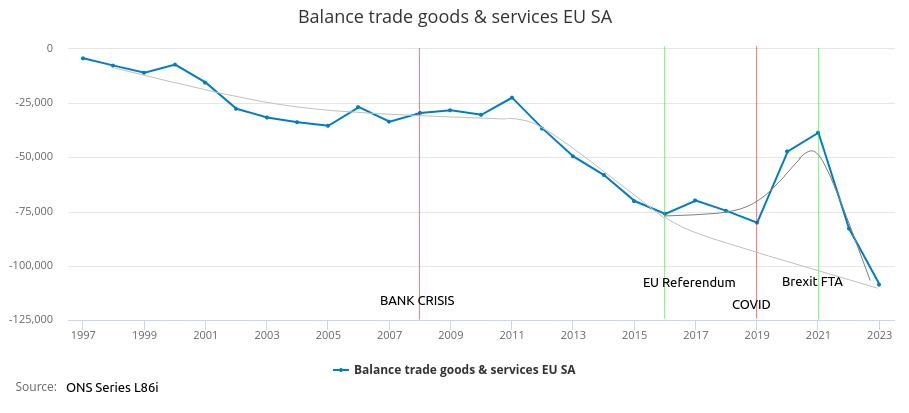

Balance of Trade in Goods and Services with EU (Series l86i):

The uncertainty after the Referendum seems to have slightly favoured exports to the EU over imports and the restrictions during COVID increased this difference. COVID decreased service sector imports far more than it decreased service exports. The net effect of COVID was to reduce the trade deficit with the EU.

In 2022 and 2023 the UK economy seems to have returned to the underlying trend of an increasing trade deficit with the EU. About 40% of the c.£110 billion UK trade deficit with the EU is with Germany (2023 UK exports to Germany £40bn, Imports from Germany £85 bn).

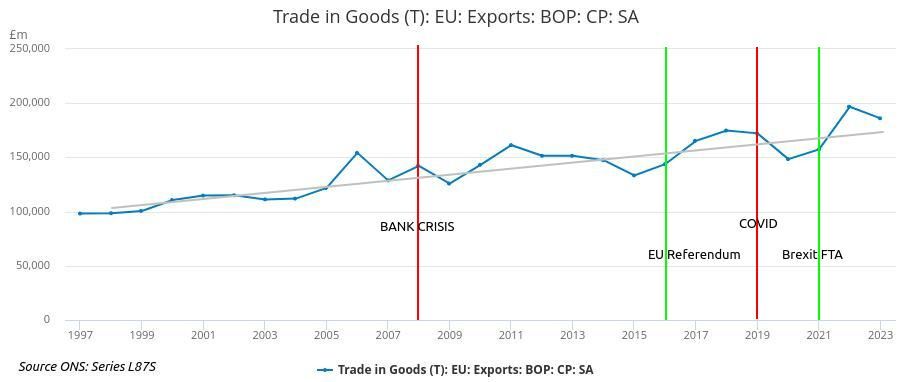

(£186 billion in 2023) These have continued on trend without a Brexit effect.

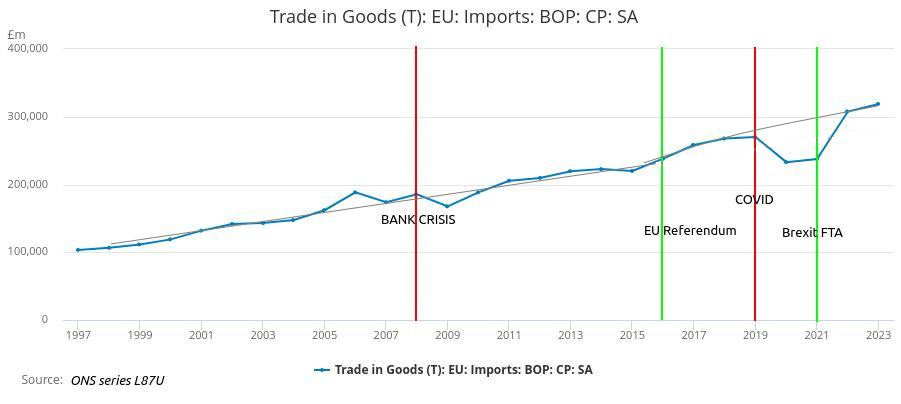

(£319 billion in 2023) Imports from the EU have been steadily increasing but on trend, again without any obvious Brexit effect:

In the service sector both imports and exports have increased by similar amounts. This is “off trend” but not related to Brexit unless Brexit favoured both service imports and exports.

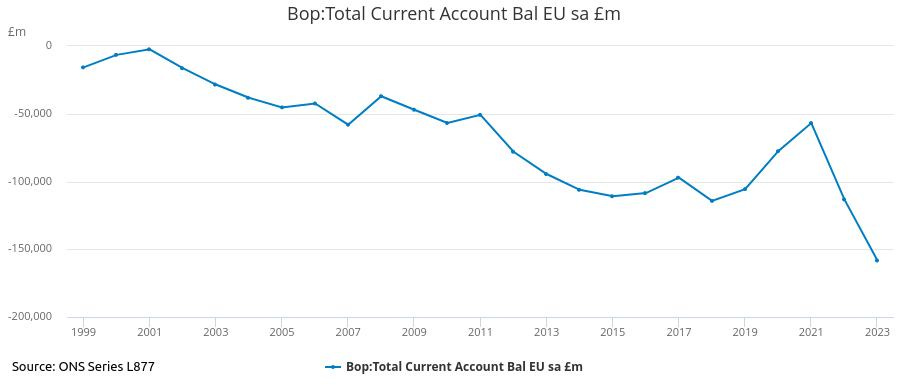

Balance of Payments Current Account with EU :

The Balance of Payments Current Account is derived from trading and short term financial transactions with the EU. These are trade in goods and services plus rents, dividends etc., remittances and profits sent between the EU and UK. The total deficit was £158 BILLION in 2023 alone. The government has found it necessary to take out loans and sell property and businesses to foreigners to pay for this deficit because, without such sales the pound will fall. A falling pound would automatically adjust the balance of payments back to zero but would have other detrimental consequences for several years because we currently have a high standard of living through paying for goods by selling our assets and borrowing. No one cares about the children of the current population who will inherit the debts and be deprived of the assets.

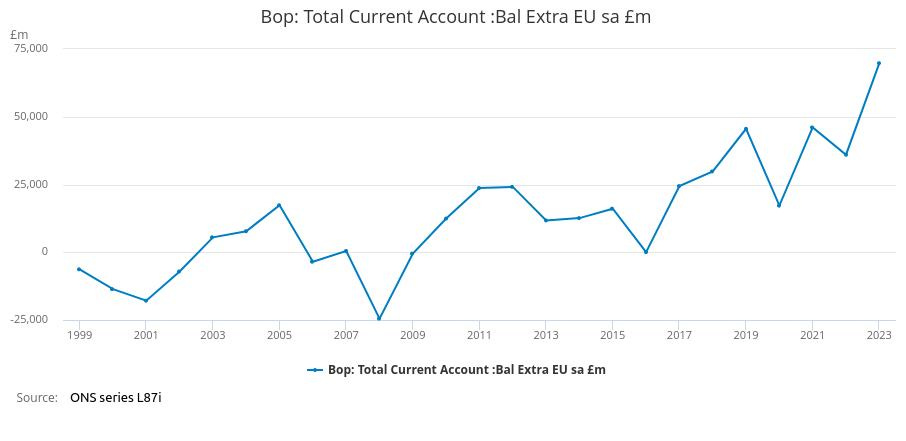

The Current Account Balance with non-EU countries was very healthy at almost £70 Billion surplus in 2023.

The Current Account Balance with non-EU Countries:

The data show that the Free Trade Agreement with the EU has normalised UK-EU trade. It is continuing the slide into ever increasing deficit.

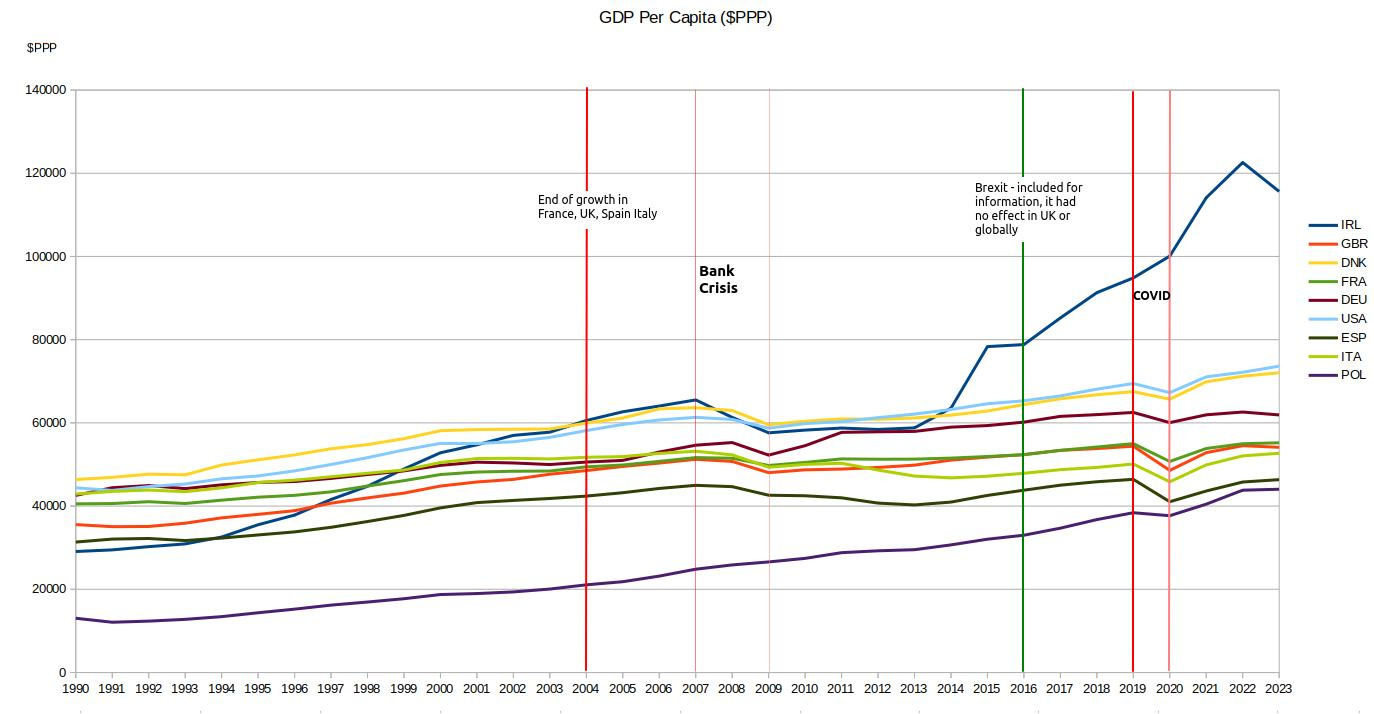

Since 2011 the UK has followed the same economic pattern as France, Italy, Spain and Germany, as can be seen from the real GDP per capita figures:

Source: World Bank Databank: World Development Indicators

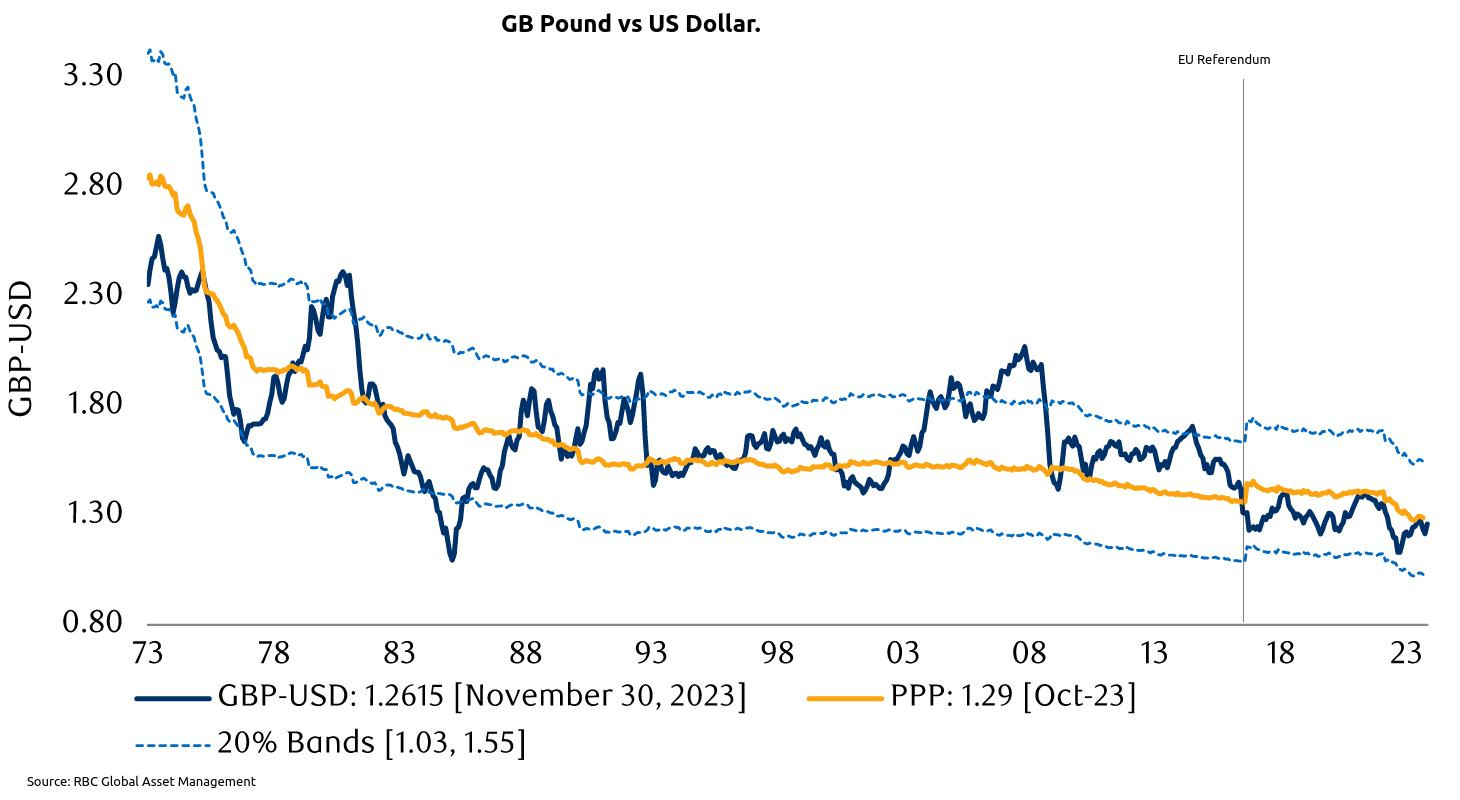

The value of the pound has also been scarcely affected by Brexit. This might come as a surprise to many readers who were influenced by UK mainstream media.

Source: RBC Global Asset Management If you cannot believe this chart because it contradicts what you heard in the media see others such as the Macrotrends GBP-USD chart.

The Royal Bank of Canada graphic above also shows the Purchase Power Parity (PPP) value of the pound in yellow as well as the exchange rate in navy blue. The PPP figure is based on the actual purchasing power of a currency - how many dollars or pounds are needed to buy a basket of goods and assets. In the long term this governs the value of a currency. The sudden, but relatively small, step up in the PPP value of the pound in 2016 is a clear indication of the artificial speculation against the pound by major banks to create the story of the drastically ‘falling pound’. The pound has now settled to its long term valuation set by the huge fall created by joining the EEC in 1973.

The economic objective of those who desire to rejoin the EU is to increase international trade volumes because this increases the prosperity of multinational corporations. This will not make us any richer but will shift production from domestic industries to the multinational companies that profit from international trade. It is surprising that the health of multinational corporations and international banks was a major factor behind the Remain vote in 2016:

Source: Lord Ashcroft Polls

It is breathtaking that Investment in the UK by International Companies (which damages the economy) was considered more important than the ability to control our own laws by half the UK electorate.

Given the figures above it is astonishing how effective the UK media have been at giving the impression that Brexit was an economic disaster. Overall Brexit had very little effect and the Free Trade Agreement allowed business to continue as usual. Although “overall” Brexit had little effect some industries did badly and some did well, the media only cover those that did badly.

The overall economic effect of Brexit was minimal compared with Remaining in the EU. The Free Trade Agreement has ensured that it is “business as usual”.